Catering Cash Flow Management: A 2026 Guide

How to manage catering cash flow in 2026: treat deposits as liabilities, build 15–20% reserves, run a 13-week forecast, and invoice fast to avoid cash-flow whiplash.

Catering cash flow management is the process of controlling the timing and amounts of money coming in and going out of a catering business to keep it financially stable and operationally efficient. Most caterers earn revenue in uneven bursts tied to events, seasons, and bookings. That pattern creates a dangerous gap between when you spend money and when you actually collect it.

Poor cash flow timing is the leading cause of catering business closures in 2026. Understanding how to manage catering cash flow means mastering deposits, reserves, forecasting, and expense timing before a cash crunch forces a crisis decision.

What is catering cash flow management, and why does it matter?

Catering financial management differs from standard business accounting because revenue arrives in irregular waves. You might book ten weddings in spring, collect deposits in January and February, then spend heavily on food, staff, and rentals in April and May before final payments arrive. That gap between outflow and inflow is where businesses fail.

Cash-flow whiplash is the term for what happens when deposits and final payments are out of sync with operating costs. It threatens solvency even in profitable businesses. A caterer can show strong annual revenue on paper while running out of cash to pay a produce supplier on a Tuesday morning.

The standard industry term for addressing this is cash flow management, and it applies to catering with specific urgency because of event-driven revenue cycles. Unlike a retail store with daily sales, a catering business may go weeks with no inflows while fixed costs like rent, insurance, and salaried staff continue. Recognizing this structural mismatch is the first step toward fixing it.

What are the main components of catering cash flow?

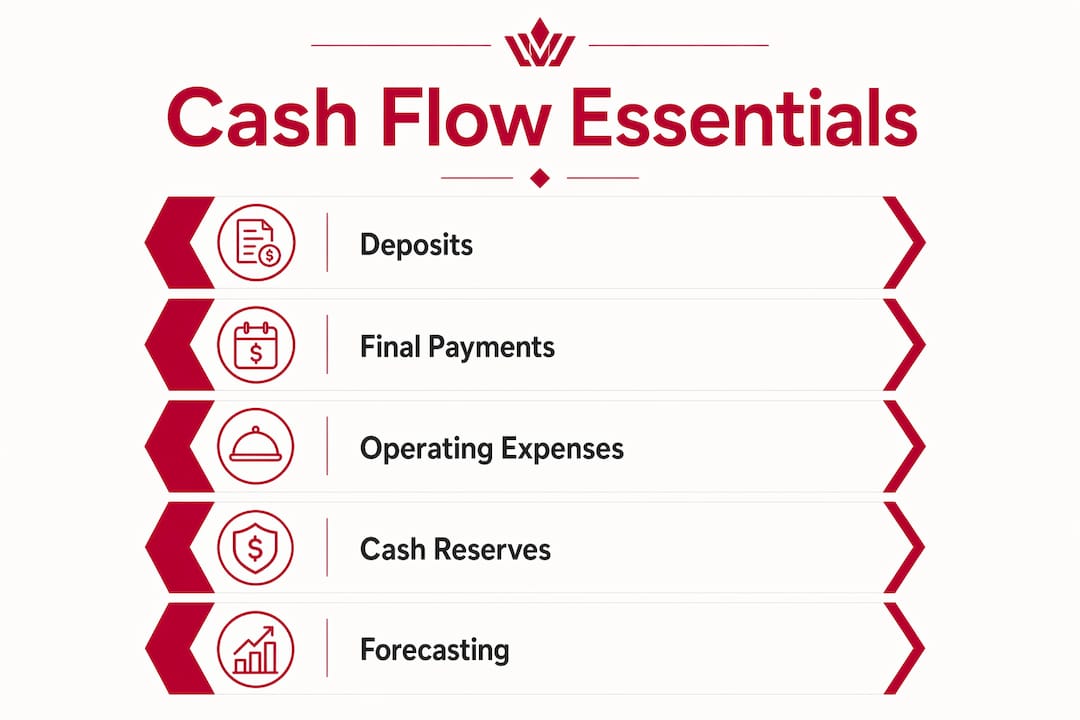

Every catering cash flow model has four core elements: deposits, final payments, operating expenses, and cash reserves. Each one plays a distinct role in keeping the business liquid.

Deposits are the most misunderstood component. Professional caterers require deposits ranging between 25% and 50% of the event total. These deposits are not income — they are contract liabilities that fund upfront food purchasing and operational costs. Treating a deposit as profit before the event is complete causes liquidity shortages when the actual costs arrive.

Final payments close the revenue cycle for each event. The timing of final payment collection directly affects your weekly cash position. Slow invoicing after an event means you carry the cost of goods sold without reimbursement, sometimes for weeks.

Operating expenses fall into three main categories:

- Payroll. Labor is typically the largest cash outflow and hits on a fixed schedule regardless of event volume.

- Food purchasing. Ingredient costs spike before events and must be paid before revenue is collected.

- Fixed costs. Rent, utilities, insurance, and equipment leases continue through slow months with no adjustment for lower revenue.

Cash reserves are the buffer that keeps all of the above from collapsing during off-season periods. Setting aside 15% to 20% of peak-season revenue into a dedicated reserve account covers fixed costs when bookings dry up.

Pro tip: Open a separate bank account specifically for cash reserves. Keeping reserve funds in your operating account makes them invisible and easy to spend accidentally.

How do caterers forecast and monitor cash flow effectively?

Forecasting is the practice of mapping future cash inflows and outflows before they happen. Without it, you react to shortfalls instead of preventing them.

The 13-week rolling forecast

The 13-week rolling cash flow forecast, updated weekly, is the gold standard for catering businesses. It gives you a 90-day forward view of your cash position at any given time. Each week, you update the forecast with actual results and extend the window by one week. This keeps the model current and replaces crisis management with proactive planning.

Building the forecast requires three inputs:

- Confirmed bookings and deposit schedules. Pull every confirmed event, its deposit amount, and its expected final payment date. These are your inflow anchors.

- Fixed and variable expense schedules. Map payroll dates, rent due dates, supplier payment terms, and any known large purchases. These are your outflow anchors.

- Historical seasonality data. Use prior years to estimate inquiry volume, booking conversion rates, and revenue by month. This fills in the gaps between confirmed events.

Cash calendar visualization

A cash calendar translates your forecast into a visual format showing week-by-week cash balances. It makes lumpy inflows and outflows visible at a glance. When you see three consecutive weeks of net outflows in October, you can act in August rather than scrambling in October.

| Forecast tool | Primary use | Update frequency |

|---|---|---|

| 13-week rolling forecast | Predict shortfalls 90 days out | Weekly |

| Cash calendar | Visualize inflow and outflow timing | Monthly |

| Receivables aging report | Track unpaid invoices by days outstanding | Weekly |

Separating corporate and social event tracking

Corporate catering invoicing operates on net-30 or net-60 payment terms, which creates receivables gaps that social event deposits do not. Tracking these two revenue streams separately prevents you from assuming corporate revenue is available when it is still 45 days from collection.

Pro tip: Build the cost of float into your corporate catering pricing. If you are waiting 60 days for payment, that delay has a real cost — price it in, or require a deposit to offset it.

What strategies minimize cash flow risks unique to catering?

Catering cash flow strategies work best when they are built into your standard operating procedures, not applied as emergency fixes.

"Successful caterers treat cash flow like a menu item. It requires the same deliberate design as your service offerings."

The most effective risk-reduction strategies for caterers are:

- Require deposits at booking. Never begin event planning without a signed contract and a deposit in hand. Deposits treated as contract liabilities ensure you have cash to cover cost of goods sold before profit is realized.

- Build and protect cash reserves. Reserve 15% to 20% of peak revenue in a dedicated account. Treat it as untouchable except for covering fixed costs during slow periods.

- Spread bookings intentionally. Avoid clustering all large events in the same two-week window. Spreading events across the calendar smooths both inflows and outflows, reducing the risk of a single cancellation creating a cash crisis.

- Control inventory with par levels. Over-ordering ties up capital and harms cash flow. Set par levels for common ingredients and order based on confirmed event data, not estimates. Just-in-time ordering frees cash for payroll and emergencies.

- Invoice immediately after events. Every day you delay sending a final invoice is a day your cash position worsens. Automate or schedule invoicing to go out within 24 hours of event completion.

Catering budget management also means reviewing your service mix. High-margin corporate lunch programs generate smaller but more frequent and predictable cash inflows. Large social events generate bigger but less frequent and less predictable inflows. A deliberate mix of both stabilizes your monthly cash position.

How does strong cash flow management affect catering success?

Good catering financial management does more than prevent bankruptcy — it changes how you make every operational decision.

When your cash position is visible and predictable, you can negotiate better payment terms with vendors. Suppliers offer discounts for early payment, sometimes 2% for paying within 10 days instead of 30. That discount compounds across hundreds of purchases per year. Caterers with healthy cash reserves capture those savings; caterers running tight do not.

Cash flow visibility also informs hiring and equipment decisions. Buying a new oven or hiring a full-time sous chef is a different decision when you can see your cash position 90 days forward. You either confirm you have the capacity to absorb the cost or you delay until you do.

Seasonal demand swings are survivable with proper reserves and forecasting. A caterer who builds reserves during a busy summer can pay rent, insurance, and a skeleton crew through a slow January without taking on debt. One who does not build reserves faces the same slow January with the same fixed costs and no buffer.

The importance of cash flow in catering extends to client relationships as well. A business under cash pressure makes reactive decisions: cutting portion sizes, delaying supplier payments, or accepting low-margin bookings just to generate cash. None of those decisions serve your clients or your reputation.

Key takeaways

Effective catering cash flow management requires treating deposits as liabilities, forecasting 90 days forward, and building reserves before slow seasons arrive.

| Point | Details |

|---|---|

| Deposits are liabilities, not income | Treat deposits as restricted funds covering event costs before any profit is recognized. |

| Use a 13-week rolling forecast | Update your cash forecast weekly to spot shortfalls 90 days before they become crises. |

| Reserve 15%–20% of peak revenue | Set aside peak-season earnings in a dedicated account to cover fixed costs in slow months. |

| Separate corporate and social tracking | Corporate net-30/60 terms create receivables gaps that need separate monitoring and pricing. |

| Control inventory with par levels | Order ingredients based on confirmed event data to free up cash for payroll and emergencies. |

Cash flow is a discipline, not a spreadsheet

I have worked with caterers who run genuinely excellent operations — great food, loyal clients, strong reputations. And some of them nearly went under, not because of bad cooking, but because they treated cash flow as a bookkeeping task rather than an operational discipline.

The mistake I see most often is depositing event deposits directly into the operating account and spending them. It feels fine until the event arrives and the food bill, the rental invoice, and the staffing costs all land at once. Suddenly the deposit is gone and the final payment has not arrived yet. That is cash-flow whiplash in real time.

What actually works is building cash flow rules into your booking process from day one. Deposits go into a restricted account. Reserves are funded automatically as a percentage of every deposit received. Invoices go out within 24 hours of event completion. These are not complicated systems — they are habits that compound over time.

The caterers I respect most also think about their booking mix the way a portfolio manager thinks about asset allocation. They balance high-margin corporate events with social bookings to smooth monthly cash inflows. They know which months are structurally weak and plan for them in advance rather than hoping for a late booking surge.

Forecasting is not about predicting the future perfectly. It is about giving yourself enough warning to act. A 13-week rolling forecast does not need to be exact — it needs to be current and honest. Update it every week, look at the weeks where cash goes negative, then do something about it before those weeks arrive.

— Kareem

How Edesia helps caterers stay on top of their finances

Managing bookings, deposits, and client communication takes time that most caterers do not have. Every missed inquiry or delayed booking confirmation is a gap in your cash flow before the event even starts.

Edesia is an AI catering assistant that handles client calls, texts, and emails instantly, so bookings are confirmed and deposits are collected without delay. Edesia also generates shopping lists directly from confirmed events, which supports just-in-time ordering and reduces inventory over-spending. When your booking pipeline is organized and your client communication is handled, your cash flow forecast has better data to work with — which means fewer surprises and more time in the kitchen where it matters.

Frequently asked questions

What is catering cash flow management?

Catering cash flow management is the practice of tracking and controlling the timing of money coming in and going out of a catering business. It includes managing deposits, final payments, operating expenses, and cash reserves to maintain financial stability across seasonal and event-driven revenue cycles.

How much deposit should caterers require?

Professional caterers typically require deposits between 25% and 50% of the event total. These deposits should be treated as contract liabilities, not income, until the event is completed and costs are covered.

What is a 13-week rolling cash flow forecast?

A 13-week rolling forecast is a 90-day forward view of your cash position, updated every week with actual results. It replaces reactive crisis management with proactive planning by showing cash shortfalls before they arrive.

How do caterers handle slow seasons financially?

Caterers cover slow-season fixed costs by setting aside 15% to 20% of peak-season revenue into a dedicated cash reserve account. This reserve funds rent, insurance, and payroll during low-booking periods without requiring debt.

Why does inventory management affect cash flow?

Over-ordering ingredients ties up cash in stock that may not be used, reducing the funds available for payroll or urgent expenses. Par-level and just-in-time ordering based on confirmed event data keeps cash available and reduces waste.

Run your catering on autopilot

Edesia is an AI assistant for caterers, food trucks, and private chefs — it answers every call, text, and email, sends your price, and books the date, so you never miss a booking.